August 7, 2023

Public relations firm inks lease at new development

Locust Street Group, a D.C.-based public affairs and communications firm, has inked a lease for a new headquarters. The company, now based at 2008 Hillyer Place NW, will soon relocate to 21,500 square feet at the Herald building, 1307 New York Ave. NW, under a 12-year lease for a floor and a half.

The Herald is “a long-term home that creates a sophisticated, warm and unique space,” David Barnhart, founding partner and CEO of LSG, said in a statement. Locust Street group, founded in 2008 and with branch offices in four other major U.S. cities, works in brand building, reputation management and influencing public opinion and counts trade associations, political groups and businesses as clients.

The 114,000-square-foot former home of the Washington Times-Herald has landed a spate of tenants since New York-based Marx Realty completed a major renovation a few years ago. Financial services consulting firm FS Vector and the Society of Industrial and Office Realtors each also inked leases earlier this year.

Ken Biberaj and Danielle Ferrari of Savills represented Locust Street Group, opposite Will Stern and Eli Barnes of Avison Young.

This Week’s D.C. Deal Sheet

Marx Realty has landed a 21.5K SF lease with Locust Street Group at The Herald office building in Downtown D.C. The strategic communications and public relations firm committed to a 12-year lease for the full 10th floor and more than half of the ninth floor.

The New York-based developer acquired the building at 1307 New York Ave. NW in April 2020, then completed a $41.5M renovation, designed by Studios Architecture. Avision Young’s Will Stern and Eli Barnes represented the landlord in the lease, while Savills’ Ken Biberaj and Danielle Ferrari represented the tenant.

PR Firm Locust Street Group Inks 22K SF at The Herald

August 4, 2023

Locust Street Group has inked a 12-year lease at The Herald, the restored former home of the Washington Herald Examiner in Washington, D.C.

The public affairs firm will take 21,500 square feet, spanning the entire 10th floor and half of the ninth floor in the 114,000-square-foot office property. The company is relocating its D.C. offices from 2008 Hillyer Place NW.

Marx Realty acquired the historic building in 2020 for $41 million, which held both the Washington Herald Examiner’s offices and printing presses, to which it owes the 19-foot ceilings on the ground floor. It’s there that Jaqueline Kennedy Onassis started her career as a photographer and reporter.

Located at 1307 New York Avenue, the building was built in 1923 and is known for its Beaux Arts style infused with a luxury hotel sensibility. The building features a new 40-seat boardroom, a European-style cafe and the Bouvier Club, an 8,800-square-foot lounge that incorporates historic photos, curated artwork, newspaper-printing memorabilia and a fireplace.

“The remarkable and prestigious tenant roster at The Herald is a testament to its distinctive hospitality-infused aesthetics, creating an inspiring environment that seamlessly blends modern amenities with the building’s rich historical charm,” Craig Deitelzweig, CEO of Marx Realty, said in a prepared statement.

Locust Street Group was represented by Ken Biberaj and Danielle Ferrari of Savills, while Avison Young’ Will Stern and Eli Barnes handled things for the landlord.

August 1, 2023

Financial market maker GTS will keep its offices at 545 Madison Avenue.

The global trading firm signed a two-year lease extension for its 30,094-square-foot offices spread across four floors at the 17 story building, according to landlord Marx Realty.

Asking rent was $100 per square foot, Craig Deitelzweig, CEO and president of Marx Realty, wrote in an email to Commercial Observer. Marx Realty handled the deal in-house, and GTS had no brokers.

GTS has occupied 545 Madison on the corner of East 55th Street and Madison Avenue for roughly 10 years, Deitelzweig said, and was initially drawn to the building for its “prime Plaza District location”.

The building has undergone quite the facelift over the past few years. During the height of the pandemic, the building saw renovations to its lobby, including the addition of a uniformed doorman and a library, as well as small upgrades such as “refined mood music, soothing lighting, and a signature scent,” according to Marx.

GTS – which also has an office at 40 Wall Street – was “particularly impressed with the renovations to 545’s lobby, Deitelzweig wrote, explaining that the upgrades influenced GTS’s decision to extend its lease.

GTS did not respond to a request for comment. – Leah Breakstone

Locust Street Group Signs 21,500 SF Lease at Marx Realty’s The Herald in DC

Strategic Communications and Public Affairs Firm Takes Tenth Floor and More Than Half of Ninth Floor at Hospitality-Infused Office Building

AUGUST 4, 2023

Marx Realty (MNPP), a New York-based owner, developer and manager of office, retail and multifamily property across the United States, announced strategic communications and public affairs firm Locust Street Group (LSG) has signed an approximately 21,500-square-foot, 12-year lease at The Herald in Washington, DC. The firm will take the full 10th floor and more than half of the 9th floor at the building located at 1307 New York Ave.

“We are thrilled to welcome LSG to the building,” said Craig Deitelzweig, CEO of Marx Realty. “The remarkable and prestigious tenant roster at The Herald is a testament to its distinctive hospitality-infused aesthetics, creating an inspiring environment that seamlessly blends modern amenities with the building’s rich historical charm. We are confident the exceptional and inspiring design sensibility here will give LSG and its associates a workplace experience that will set the stage for future growth and success.”

The award-winning Herald sets a precedent as the first office building in Washington, DC to embrace a hospitality-infused aesthetic, blending a New York club-like vibe with the sophistication of a DC design sensibility. Originally constructed in 1923 and acquired by Marx Realty in 2020, this 114,000-square-foot building showcases a distinct Beaux Arts style infused with a luxury hotel sensibility, bringing a fresh and innovative workplace concept to the DC market. Every intricate detail pays homage to its past as the former home to the offices and printing presses of the Washington Times-Herald where the legendary Jaqueline Kennedy Onassis (then Bouvier) began her career as the “Inquiring Camera Girl,” both as a photographer and reporter.

“We are extremely proud of the impactful work LSG is doing for clients and we are thrilled to partner with The Herald to create a long-term home that creates a sophisticated, warm and unique space for our amazing team members,” said David Barnhart, founding partner and CEO of LSG. “We are looking forward to welcoming our employees and our clients into our new, beautiful space at the building. We’re excited for this next chapter and can’t wait to see what we’ll be able to achieve in an environment designed to inspire creativity, foster collaboration and also provide more optionality and comfort to our team. With its hospitality-infused ambiance and blend of history and modern timelessness, The Herald as it provides the perfect backdrop for our team to thrive and grow.”

The Herald’s experience starts at the entry with its welcoming portal, intimate foyer, and expansive lobby designed to evoke its newspaper office and production heritage. Adorned with walnut wood, copper accents, plush seating areas, and soaring ceilings, the building and its design details capture Jackie O’s timeless grace and sophistication. A uniformed doorman attends oversized wooden entry doors as The Herald welcomes tenants and guests with mood music and Marx Realty’s signature scent, blurring the lines between a commercial building and a luxury hotel.

The exceptional amenities at The Herald include a 40-seat boardroom, European-style café, and the Bouvier Lounge – a meticulously curated 8,800-square-foot club floor featuring historic photos, artwork, newspaper printing memorabilia, and a fireplace. Additionally, tenants now have access to the groundbreaking Marx Mobile, a 2023 Tesla Y. The building’s branded house car provides transportation around DC and is available for tenants via the MarxConnect app. The well-appointed fitness center, Press Fitness, offers boxing facilities, private workout rooms featuring individual pelotons, Hydrow rowers, and Mirror fitness system with historically significant and modern artwork throughout.

The Herald is the result of the ongoing successful collaboration between Marx Realty and Studios Architecture, continuing the hospitality-meets-office repositioning success at 10 Grand Central and 545 Madison Avenue, both in New York City.

LSG was represented by Ken Biberaj and Danielle Ferrari of Savills. Avison Young is the leasing agent of the building, with a team headed by Will Stern and Eli Barnes.

Office Struggles Persist; Cushman Takes Lead

Large office sales in the first half tumbled to a low not seen in more than a decade as headwinds continued to batter the beleaguered sector, dashing hopes for a quick recovery.

In the first six months, just $15.34 billion of office properties valued at $25 million or more changed hands, a 67% decline from the same period in 2022, according to Green Street’s Sales Comps Database. That’s the weakest first half recorded since 2010, when sales dipped to $10.41 billion in the aftermath of the global financial crisis.

The top five brokerages all registered substantial drops in brokered deals, scram- bling the typical lineup of rankings at the midway point. Cushman & Wakefield landed in first place with $2.43 billion of sales, down 66% year over year, while JLL, in second, saw a 72% fall in activity to $2.08 billion. CBRE, which typically jock- eys for first place, narrowly placed third with $1.86 billion of trades, an 82% drop. Newmark came in fourth, with $1.85 billion of trades (see article on Page 13), while

Eastdil Secured, also a perennial contender for the top spot, tumbled to fifth with $1.61 billion of sales. Both firms’ activity was down 79% versus the first half a year ago.

The conditions that started the slump last year continue to weigh on the sector, namely cloudy leasing demand and scarce and costly debt. Those factors have pushed the asset class out of favor with buyers and made valuing office properties nearly impossible. Pros believe there will be a recovery — but it will take time.

“This is the storm of the century for office,” said Doug Harmon, co-head of U.S. capital markets for Newmark. “Values are resetting, and until there is more clarity on all the variables negatively impacting the asset class, trading volumes will remain muted. If the economy stays resilient, inflation is tamed and interest rates stabilize — all of which are now probable — then the death of office will have been greatly exaggerated and trading of repriced office assets will return with gusto.”

But no one expects those issues to be resolved this year, meaning the second half also likely will be slow for sales activity. For now, “we are bouncing on the bottom,” said Chris Ludeman, CBRE’s global president of capital markets.

Deals that did cross the finish line in the first half tended to be smaller than usual. Nationwide, just 243 office transactions closed from January through June, nearly a third of the 733 deals that wrapped up during the first six months of 2022, according to the database. Just 38 deals valued at $100 million or more traded in the first half, compared with 116 last year. Only four sales surpassed $500 million as of June 30, down from 14 during the first six months of 2022.

The first half was also the first January-June period since 2012 when the average deal size slipped below $100 million, according to the database. The average transaction in the first six months was $84.7 million, down from $113.6 million during the same period last year. The 10-year peak came in the first half of 2021 at $121.6 million.

Ludeman likened the sector’s expected trajectory to that of retail — when the rise of e-commerce sent a seismic wave through the industry, stifling property sales for years. Similarly, office owners are adjusting to systemic changes in leasing demand stemming from the sticky work-from-home trend that took hold during the pandemic. Investors and lenders won’t return until that improves. “The [performance] fundamentals will lead us to a better day, but that is not today,” Ludeman said.

The leasing market started to show signs of improvement in the second quarter, though overall occupancy still dropped. “There are quite a few green shoots,” said Mark Katz, a senior managing director and co-head of JLL’s national office-invest- ment sales group. He said more firms are moving workers back to offices, which should eventually spur leasing demand.

While net absorption in April through June remained negative nationwide, as tenants vacated 12.5 million sf of space, that was down from 20 million sf vacated in the first three months of the year, according to JLL. While leasing activity was insufficient to cover the growing vacancy, it was up 11.6% in the second quarter over the first.

The lack of clarity surrounding the performance of office properties has prompted lenders to shy away from originating debt on all but the most core, trophy assets. The upshot: “Almost every transaction has to be [financed with] existing financing or seller financing,” JLL’s Katz said. “Until the debt markets recover, we are not going to have a recovery [in office sales].”

That also means a continued lack of visibility on valuations.

As the hardest hit asset class since the start of the pandemic, “there is much debate with regard to how much office values have fallen thus far and how much more they may have left to fall,” Green Street, the parent of Real Estate Alert, said in a July report.

Those sales that are happening are largely the result of distress, when owners unable to refinance or fund capital improvements to boost leasing are forced to cooperate with lenders to exit investments. In other cases, they sell properties to raise liquidity to address other balance-sheet issues. For the handful of players still active in the space, that spells opportunity.

“We can start to buy income again at higher yields and lower risk,” said Joe Gorin, a managing director and head of U.S. real estate equity at Barings. Capitalization rates have increased to a point where a high-quality property can potentially stabilize above 10%. “We haven’t talked about double-digit NOI yields in office buildings since the mid-1990s,” he said.

His company closed on one of the few sizable trades of the first half, paying Alexandria Real Estate Equities $117.5 million, or $231/sf, last month for Riverside Center, a 510,000-sf office and life-science complex in the Boston suburb of Newton.

Buyers are being highly selective, focusing on properties perceived to check all the boxes that tenants require today. “You have to be very careful about what you buy at this time,” said Craig Deitelzweig, chief executive of Marx Realty. “It’s the most bifurcated [leasing] market I’ve ever seen in my lifetime. If you are not a good property with the types of amenities that tenants want, you won’t lease at any price.”

Against that backdrop, nearly every market saw a drop in sales volume. New York, the perennial leader in office sales, registered $3.02 billion of trades, down 56% year over year, followed by Boston with $2.04 billion of activity, down 45%. Washington, where early distressed buying opportunities have started to arise, was in third, with $1.23 billion of sales, a 57% decline.

West Coast markets, which had been popular with investors in recent years due to their heavy concentrations of technology- focused companies, took a beating. Sales in San Francisco were down 71% to $433.3 million, while Seattle saw just one property trade, at $34.5 million, a steep drop from $2.83 billion of total volume the year before, pushing it out of the top 20 markets altogether.

Not even Sun Belt markets, heavily favored by investors ear- lier in the pandemic due to population growth and company migration, were spared. Only Austin managed to place in the top 10 markets with $382 million of sales, a decline of 73%.

This year’s office ranking did not include sales of data-center properties, which totaled $533.6 million, down from $1.09 billion last year. CBRE dominated the niche sector with $447.3 mil- lion of trades, good for a 91% market share of brokered sales.

Broker rankings are based on property transactions that closed January through June and involved full or partial stakes valued at $25 million or more. When multiple brokers shared a listing, the dollar credit was divided evenly, but each broker was credited with one transaction. Only brokers for sellers were given credit. Portfolio transactions were included if the package price was at least $25 million.

By Simona Tudose | August 4, 2023

The tenant signed a long-term lease at 10 Grand Central.

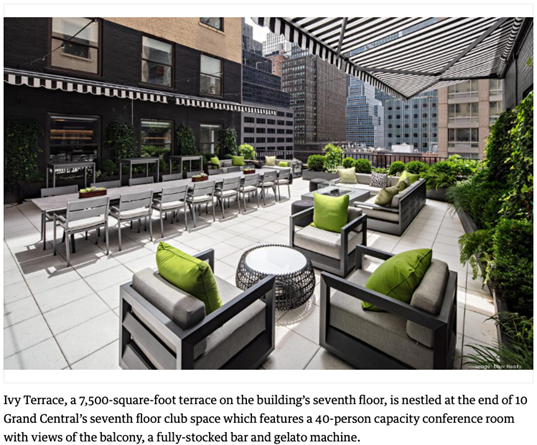

Outdoor amenity space, The Ivy Terrace

Marx Realty has signed a 10,000-square-foot, long-term lease agreement at 10 Grand Central, a 432,381-square-foot office building in Manhattan. Ohio-based LeafHome will establish its first New York City office on the Class A property’s 15th floor, to serve as its marketingheadquarters. CBRE negotiated on behalf of the tenant, while JLL represented the landlord.

Marx Realty picked up the asset in 2007 for $148.4 million, according to CommercialEdge. The company signed leases adding up to more than 90,000 square feet of space at 10 Grand Central during the past 12 months. The current tenant roster includes Merchants Bancorp, Benenson Capital Partners, MassMutual and Everside Capital Partners, among others, the same source reveals.

Located at 155 E. 44th St. within Manhattan’s Plaza District, the property includes 12 passenger elevators, 20,691-square-foot floor plates and 11,145 square feet of retail space.

A redesigned Manhattan tower

The 35-story office building recently underwent a renovation program and now features pre-built office suites, conference spaces, an oversized café island and four outdoor terraces. Marx Realty focused on implementing a hospitality package across its portfolio, with 10 Grand Central also offering services, such as a 7,500-square-foot indoor and outdoor lounge with artworks and a café, along with a 40-seat conference center.

CBRE’s Senior Associate Maxwell Tarter negotiated on behalf of LeafHome, while JLL’s team of Vice Chairman Mitchell Konsker, Vice President Kyle Young, Senior Vice President Carlee Palmer, assisted by Managing Director Simon Landman and Associate Vice President Thomas Swartz represented the landlord.

Recent deals in the borough include Empire State Realty Trust’s full-floor, long-term deal with Capco at the Empire State Building, as well as Jack Resnick & Sons two lease renewals totaling 108,086 square feet at One Seaport Plaza.

Deals of the Day: Aug. 3August 3, 2023

J. HUGHES | MARIO MARROQUIN | EDDIE SMALL

Leases

Gutter protection company inks lease for marketing headquarters in Midtown

Address: 10 Grand Central, Manhattan

Landlord: Marx Realty

Tenant: LeafHome

Lease size: 10,000 square feet

Lease length: 5.5 years

Asking rent: $92 per square foot

Asset type: Office

Brokers: CBRE’s Maxwell Tarter represented the tenant, and JLL’s Mitchell Konsker, Kyle Young, Carlee Palmer, Simon Landman and Thomas Swartz represented the landlord.

August 3, 2023

By Julian Nazar – Staff Reporter, New York Business Journal

Leaf Home, a Hudson, Ohio-based provider of home improvement products, will be opening its first New York City office at Midtown office tower 10 Grand Central in September.

This deal continues the strong leasing momentum at Marx Realty’s office property.

In the past year, more than 90,000 square feet of ground-floor retail and office space has been leased at 10 Grand Central.

“We have seen more activity in terms of leasing and tours than any other property in the Grand Central neighborhood,” Marx Realty’s CEO and President Craig Deitelzweig said in a statement. “The leasing velocity around 10 Grand Central has remained steady during the current office cycle due to the highly differentiated product offering here and across our portfolio.”

Notable amenities at the property include a 7,500-square-foot indoor/outdoor lounge and club floor with an outdoor space called “the Ivy Terrace” as well as a luxury electric Porsche Taycan that tenants can use for transportation around Manhattan.

Leaf Home is the latest company to be attracted by the amenity offerings.

The company will occupy 10,000 square feet in a pre-built space on the 15th floor of the building that includes four private outdoor terraces.

The lease is for five-and-a-half years and asking rent was $92 per square foot.

The space will serve as headquarters for Leaf Home’s marketing operations. The company is known for its LeafFilter gutter protection technology.

Leaf Home was represented by CBRE’s Maxwell Tarter on the deal. Marx Realty was represented by JLL’s Mitchell Konsker, Kyle Young, Carlee Palmer, Simon Landmann and Thomas Swartz.

Asking rents at the Midtown office tower range between $68 and $120 per square foot.

LeafHome Inks 10K-SF Lease at 10 Grand Central

New York & Tri-State + Midtown New York + Retail

By: Emily Fu | August 3, 2023

Marx Realty, a New York-based property firm, has announced that LeafHome, an Ohio-based developer of LeafFilter gutter protection technology, has signed a long-term lease for a 10,000-square-foot space at 10 Grand Central in Manhattan. The space, located on the 15th floor, will serve as LeafHome’s first New York City office and its marketing headquarters.

“We have seen more activity in terms of leasing and tours than any other office property in the Grand Central neighborhood,” said Craig Deitelzweig, president and CEO of Marx Realty.

The asking rent was $92 per square foot and LeafHome was represented by Maxwell Tarter of CBRE. Marx Realty was represented by JLL’s Mitchell Konsker, Kyle Young, Carlee Palmer, Simon Landman and Thomas Swartz. Asking rents at 10 Grand Central range between $68 and $120 per square foot.